On surface, it will seem to be a very bad situation to be in, if one is not collecting monthly rent of more than what one is paying for every month for loan installments.

However, this may not be necessary a losing investment as loan installment is not entirely an expense as it comprises of loan principal and interest.

Let’s use an example to illustrate this.

Project name: Icon at Tanjong Pagar

Unit type and size: 581 sqft, one bedroom unit

Purchase price: $1.05mil

Expected conservative monthly rent: $3000

Assuming one is taking 80% loan, at 2% interest rate, 25 years loan tenure

Monthly installment: $3600 (round up to nearest hundred)

(Monthly loan interest is $1400/mth conservatively as this interest amount will get lower as the loan amount gets lesser every month)

Question:

Rent collected: $3000 is less than the monthly loan installment of $3600. Is this investment property a liability or an asset to the property owner?

Let’s crunch some numbers and do some assessments! Monthly expenses if you rent out this unit:

1) Loan interest: $1,400

2) Maintenance fees:$250

3) Rental income tax: $200 (depends on individual’s tax bracket)

4) Property tax: $200

5) Others: $200 (eg., repairs, furnishing, vacancy periods when the unit is not able to

rent out)

Sub total: $2,250

Monthly gain: $3,000 (rent collected) less $2,250: $750

Yearly gain: 12 months times $750: $9,000

Although, there’s a need to top up every month to service the installment and other expenses, this property is still able to give a positive return to the property owner as the monthly rent collected is more than enough to cover the monthly expenses.

In my last ten over years of real estate career, I had seen so many young adults who had just started out in their career, splurge on luxurious depreciating items and neglect planning financially for themselves. This can prove to be very costly to most as they are missing out on the advantages of compounding interest through investments and leveraging on longer property loan tenure when they are young.

When you buy a property at age 30 years old, you will be able to go for full loan tenure of 30 years, and keep your monthly installment low and hence there will be more positive cashflow monthly (or at least less negative monthly cashflow).

On the contrary, if you are at age 45 years old, your loan tenure will be capped at 20 years and your monthly installments will be a lot higher and you may not be able to go for as much loan as you desired.

Through proper and prudent property investments, one can make good use of the power of leveraging through mortgage loans.

For example, if you buy a $1m property, and you take a 80% loan, your downpayment is only 20% at $200,000.

So if the property appreciates by 20%, and hence the value becomes $1.2m, your returns before expenses is not just 20% but will be 100% instead (200k/200k times 100%: 100%)! And not forgetting the monthly rent you will collect, that adds up to your returns further!

The question now is that, can an average income earner be able to own a property at a young age? Well, I had seen so many successful examples over the last many years!

For illustrations sake, let’s look at a young adult at an age 28 years old earning $5,000/month. Assuming he manages to save $3,000/month. That will translates to $36,000 per year. He aims to buy an investment property at age 35 years old. Hence in seven years time, he will be able save up to $252,000, which is sufficient to place a downpayment for a $1m property. And if he has pay increment over the next few years from age of 28 years old, he would be able to save more.

Let’s assume that if along the way, he has more monthly commitments (eg., getting married, medical expenses etc.), and can only save $2000/month. Hence, by age of 35 years old, he will be only to save up to $168,000. It is still possible to accumulate more than $200,000 in savings by age of 35 years old by setting aside monies into very safe investment/savings vehicles through endowment plans or even SG bonds (up to 2.5-3% average yearly returns).

So what’s next when I have enough monies to invest in a good investment property? Time to act on it!

Let’s look at one example.

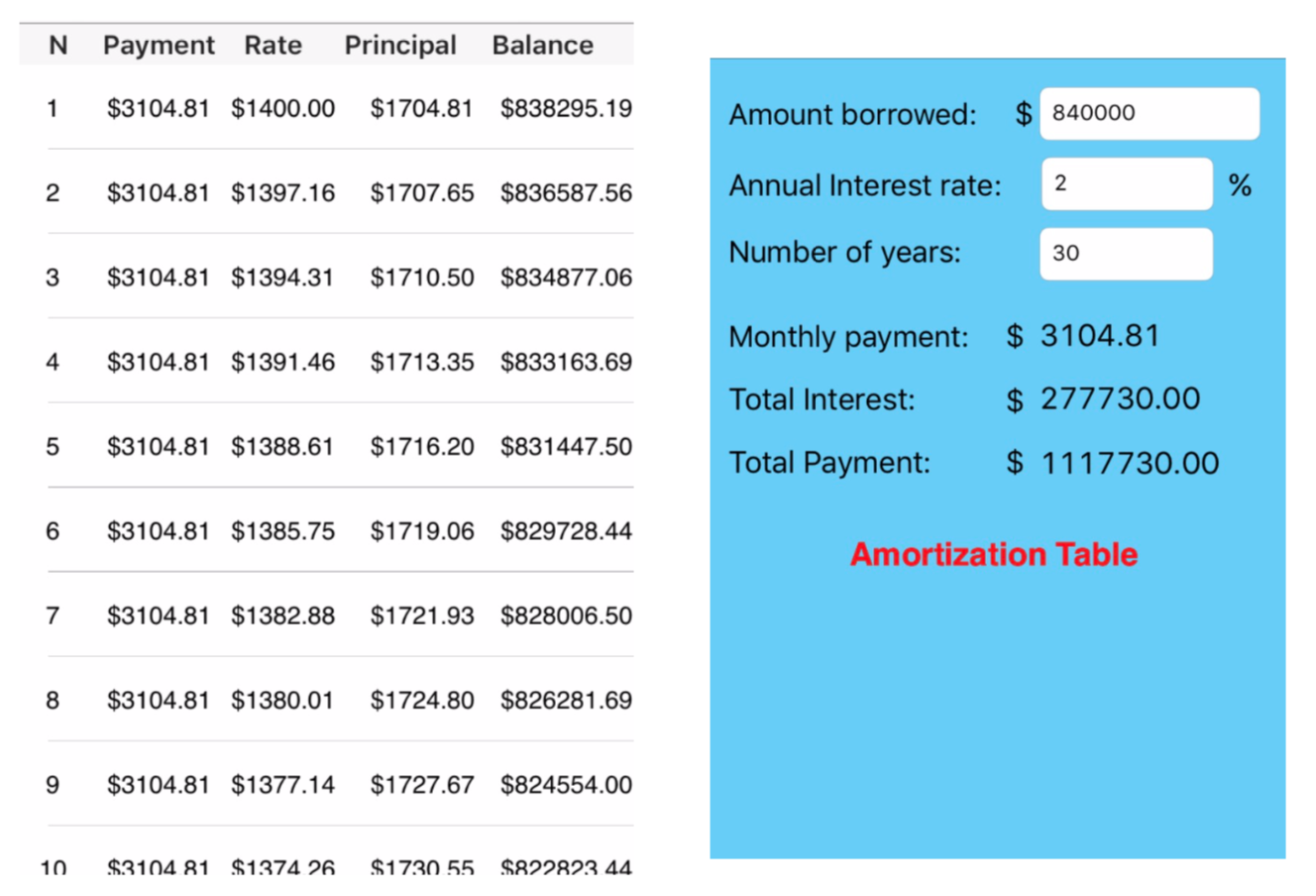

Project name: Icon at Tanjong Pagar

Unit type and size: 581 sqft, one bedroom unit Purchase price: $1.05mil

Expected conservative monthly rent: $3000 (average rent is between $3,200 to $3,500 per monthly)

Assuming one is taking 80% loan, at 2% interest rate, 30 years loan tenure

Monthly installment: $3200 (round up to nearest hundred)

(Monthly loan interest is $1400/mth conservatively as this interest amount will get lower as the loan amount gets lesser every month)

Question:

Rent collected: $3000 is less than the monthly loan installment of $3200. Is this a lousy buy or is this worth considering?

Let’s crunch some numbers and do some assessments!

Buying expenses when you first bought this unit:

1) Stamp duty: $28,000 (round up)

2) Legal fees: $3,000

3) Others: $2,000

Sub total (a): $33,000

Monthly expenses if you rent out this unit:

1) Loan interest: $1,400

2) Maintenance fees:$150

3) Rental income tax: $100 (depends on individual’s tax bracket)

4) Property tax: $200

5) Others: $200 (eg., repairs, furnishing, vacancy periods when the unit is not able to

rent out)

Sub total (b): $2,050

Monthly gain: $3,000 (rent collected) less $2,050: $950

Yearly gain: 12 months times $950: $11,400 (c)

Monthly cashflow: $3,000 rent less (items 2-5 for monthly expenses: $650) less $3,200 instalment:

($850)

Selling expenses assuming selling at price of $1,200,000 five years later (based on a mere 3% year on year price appreciation):

1) Agent commission: $26,000 (assuming 2% of selling price plus gst and round up)

2) Legal fees: $3,000

3) Others: $1,000

Sub total (d): $30,000

Total gain:

$1,200,000 (selling price) less $1,050,000 (purchase price) plus yearly gain of $11,400 (c) times 5 years less buying expenses $33,000 (a) less selling expenses $30,000 (d) : $144,000

Initial downpayment:

20% of $1,050,000: $210,000

Percentage gain on initial invested capital: $144,000/$210,000 times 100%: 68.5%

Yearly percentage gain on initial invested capital:

68.5%/5 years: 13.7%

For the above scenario, he has to ensure that he has enough savings for the negative cashflow every month of $850.

At age of 40 years when he liquidates his property, he will have $210,000 of principal and $144,000 of earnings: $354,000, which is sufficient to place a down payment for another property of $1.5-$1.7m.

Imagine that he sells off the second property again, he may be able to reap off even more profits, which may allow him to enjoy an earlier retirement very comfortably.

Of course, every investment comes with risk. As long as one does his due diligence and had set aside enough reserves to hold on to the property, property investing can be proven to be highly rewarding.

There are so many indicators/stress tests for an investor to use before choosing the right investment property to buy. And there’s no common indicator that can be used for ALL investment properties. It will be largely depending on the type of investment property one is looking at (eg., commercial, industrial, landed properties, condominiums in CBD areas versus condominiums in heartland areas etc.) and also the objective of the investor (eg. Cashflow, capital appreciation, rental yield, capital preservation etc.)

One useful indicator is as follows:

Let’s use an example to illustrate how this indicator can be used.

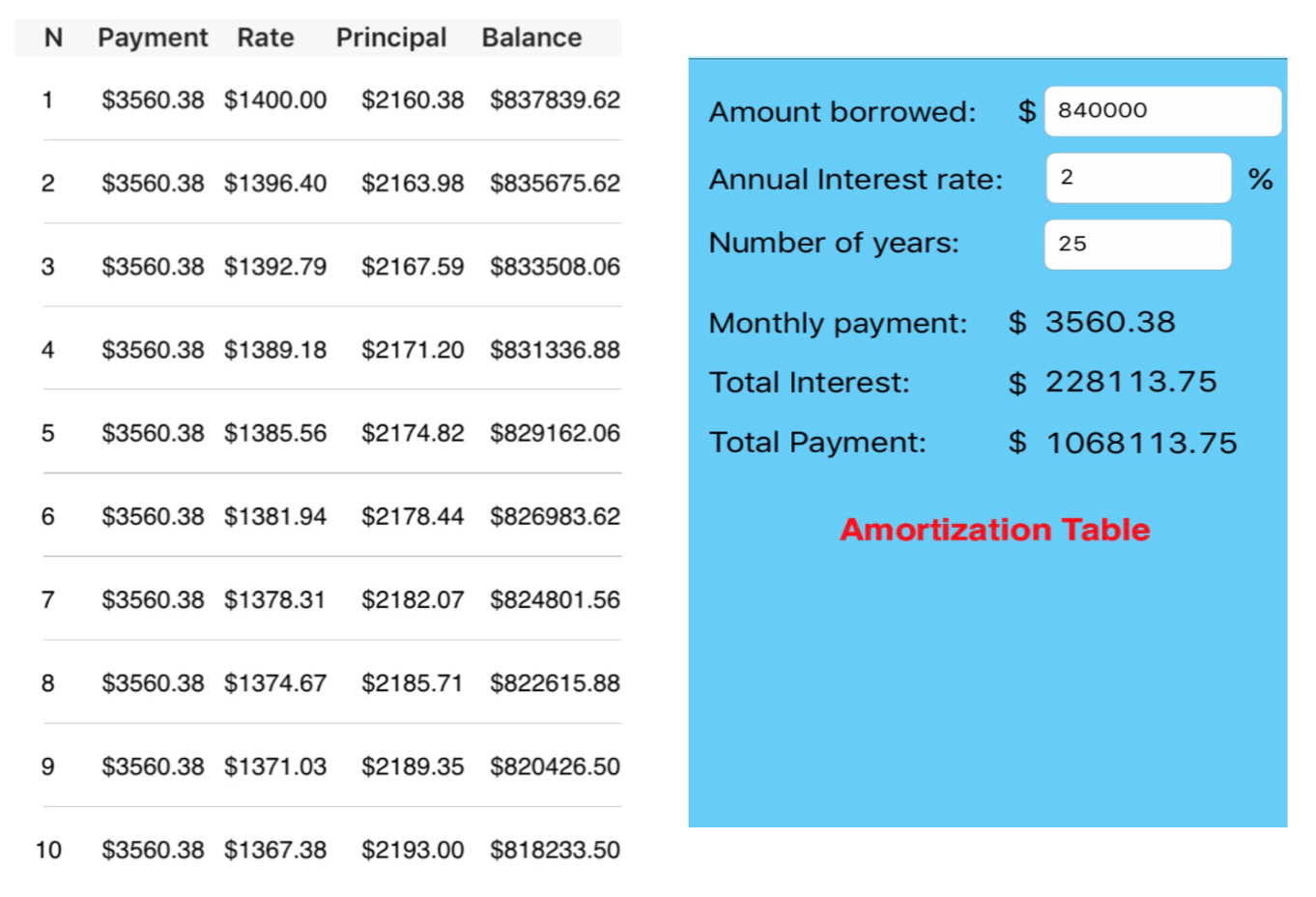

Project name: Icon at Tanjong Pagar

Unit type and size: 581 sqft, one bedroom unit

Purchase price: $1.05mil

Expected conservative monthly rent: $3000 (average rent is between $3,200 to $3,500 per monthly)

Assuming one is taking 80% loan, at 2% interest rate, 25 years loan tenure

Monthly instalment: $3600 (round up to nearest hundred)

(Monthly loan interest is $1400/mth conservatively as this interest amount will get lower as the loan amount gets lesser every month)

Question:

Rent collected: $3000 is less than the monthly loan instalment of $3600. Is this a lousy buy or is this worth considering?

Let’s crunch some numbers and do some assessments!

Buying expenses when you first bought this unit:

1) Stamp duty: $28,000 (round up)

2) Legal fees: $3,000

3) Others: $2,000

Sub total (a): $33,000

Monthly expenses if you rent out this unit:

1) Loan interest: $1,400

2) Maintenance fees:$250

3) Rental income tax: $200 (depends on individual’s tax bracket)

4) Property tax: $200

5) Others: $200 (eg., repairs, furnishing, vacancy periods when the unit is not able to

rent out)

Sub total (b): $2,250

Monthly gain: $3,000 (rent collected) less $2,250: $750

Yearly gain: 12 months times $750: $9,000 (c)

Monthly cashflow: $3,000 less (items 2-5 for monthly expenses: $850) less $3,600 installment:

($1,450)

Selling expenses assuming selling at price of $1,100,000 five years later (based on a mere $50,000 price appreciation):

1) Agent commission: $25,000 (assuming 2% of selling price plus gst and round up)

2) Legal fees: $3,000

3) Others: $2,000

Sub total (d): $30,000

Total gain:

$1,100,000 (selling price) less $1,050,000 (purchase price) plus yearly gain of $9,000 (c) times 5 years less buying expenses $33,000 (a) less selling expenses $30,000 (d) : $32,000

Initial downpayment:

20% of $1,050,000: $210,000

Percentage gain on initial invested capital: $32,000/$210,000 times 100%: 15.2%

Yearly percentage gain on initial invested capital:

15.2%/5 years: 3.04%

Breakeven price of this property if one is to sell on the fifth year: [yearly gain of $9,000 (c) times 5 years less buying expenses $33,000 (a) less selling expenses $30,000 (d): ($18,000)] + $1,050,000 (purchase price): $1,068,000

Breakeven year of this property if one is to sell at same price: [Buying expenses $33,000 (a) plus selling expenses $30,000 (d): $63,000] / Yearly gain: $9,000 (c): 7th year

Summary and analysis of this investment (just on rental yield perspective):

1) If one see more upside in this area, meaning there are many catalysts for growth (eg., Keppel area redeveloping, CBD area, proximity to MRT, high rental demand, high investors’ interests etc.), appreciating by more than $50,000 in 5 years’ time or longer would be highly possible. Do look at the historical prices too. If historically, the price of Icon unit has hit much higher than the entry price, then there may be a chance that it may hit that price again.

2) On a very conservative approach, if one is satisfied in just getting more than the returns as compared to putting monies in safe vehicles like time deposits (1-2% interest rates on average) or Singapore bonds (2-3% interest rates on average), then this investment would be ideal because even by using the most conservative way of calculating (assuming rent price remain this low throughout, marking up the monthly and the transaction expenses etc.), the yearly returns on the invested capital is already 3.04%.

3) If market price remains stagnant all the way, and the purchaser sells the property on the 7th year at the same entry price, he will not lose money!

4) Always invest only when you have enough spare cash after setting aside monies for your needs. One must be prepared to top up close to $1,500 per month assuming rent remain low at $3,000 per month.

I would consider this unit as a good investment to look into.

For those with bigger budget and/or higher risk appetites who want to invest in something of higher returns, properties like landed properties, conservation houses, condominiums in orchard or even Sentosa may whet their appetites. Assessing these properties will require a different set of indicators. Using rental yield approach will not work because these are capital play vehicles and rental yield will be very low.